The Office of Financial Sanctions Implementation (OFSI) has published guidance (the Guidance) following the publication of the Sanctions (EU Exit) (Miscellaneous Amendments) (No.2) Regulations 2024 (the Regulations) on 14 November 2024. OFSI is the body with regulatory oversight of the financial sanctions regime and is responsible for its implementation and enforcement within the UK.

BACKGROUND

Il 27 settembre 2024 è stato pubblicato in Gazzetta Ufficiale il D. Lgs. 13 settembre 2024, n. 136 (“Correttivo-ter”), terzo – e attualmente ultimo – Decreto Correttivo al Codice della Crisi d’Impresa e dell’Insolvenza.

In a recent decision, the High Court refused to grant the Financial Times access to the whole of the Secretary of State's affirmation in support of directors' disqualification proceedings against Alexander Greensill, pursuant to either CPR 5.4C or the court's inherent jurisdiction.

2024 Any questions?

IE CA 3 Holdings Ltd and IE CA 4 Holdings Ltd (Companies) were two Canadian registered companies whose directors were located outside of Canada. The Companies’ parent company, Iris Energy Limited (Iris), was listed on NASDAQ and had its registered office in Melbourne and principal place of business in Sydney, with three of its six directors located in New South Wales.

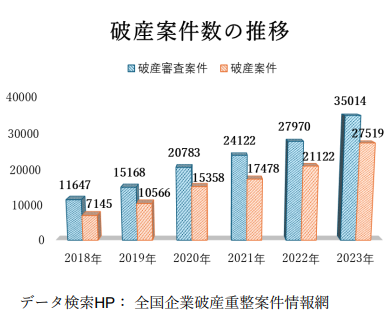

1 増加する破産案件

中国の最高人民法院は、2016年8月より「全国企業破産 重整案件情報網」というHPにおいて、全国の破産案件に 関する情報を公開しているが、当該HPにて1年ごとに破 産審査案件数及び破産案件数を検索した結果は以下の表 のとおりである。これを見ると、中国の破産案件数は近 時増加の一途をたどっていることがはっきりと見て取れ る。

http://pccz.court.gov.cn/pcajxxw/index/xxwsy

2 中国の倒産制度

Il 27 settembre 2024 è stato pubblicato in Gazzetta Ufficiale il D.Lgs. 13 settembre 2024, n. 136 (“Correttivo-ter”), è il terzo – e attualmente ultimo – Decreto Correttivo al Codice della Crisi d’Impresa e dell’Insolvenza. Il novello decreto correttivo ha apportato modificazioni sostanziali a numerosi istituti del Codice della Crisi.

On September 27, 2024, Legislative Decree No. 136 of September 13, 2024 (“Correttivo-ter”) was published in the Official Gazette. This represents the third—and currently final—Corrective Decree to the Business Crisis and Insolvency Code. The new corrective decree has introduced substantial amendments to several provisions of the Crisis Code. Beyond minor stylistic and detailed adjustments, the Correttivo-ter both incorporates certain practices or clarifies interpretive uncertainties and introduces some highly anticipated innovations for practitioners.